"For many companies, dividing the product cost from the shipping cost is a common practice in direct sales abroad. However, this procedure is often not correct."

How many times has a tourist visiting your company asked to have your alcoholic product shipped to their home?

Direct sales are one of the greatest satisfactions for an alcohol producer, but when, after the purchase, you need to ship the product abroad, precise customs and tax management is required.

The payment of excise duties, customs duties, the opening and closing of customs procedures, and the payment of VAT are governed by strict regulations. These apply not only to sales through e-commerce but also to sales from physical points of sale.

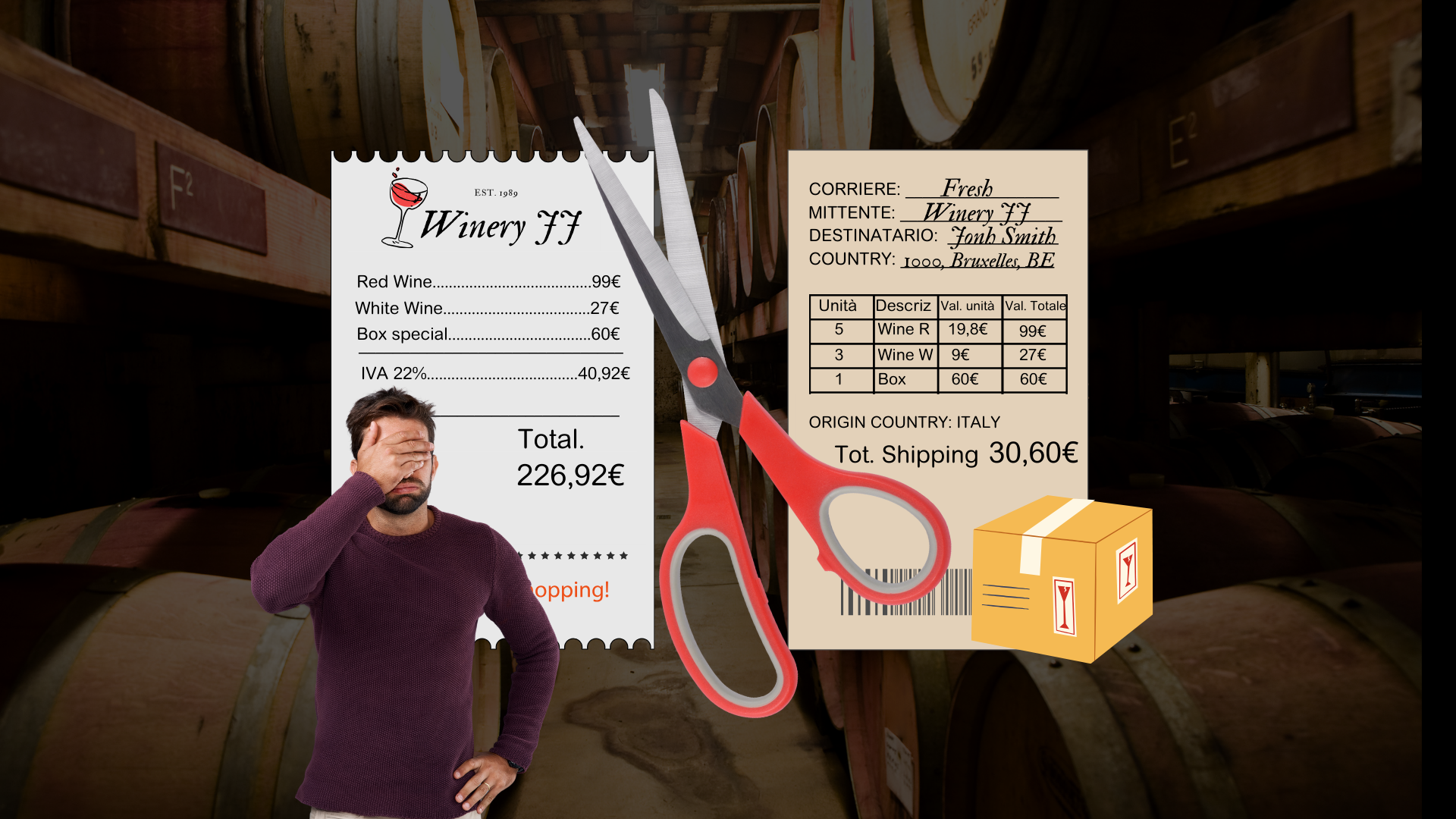

What is Split Payment in direct sales abroad?

Split payment works this way. Once a foreign tourist purchases, for example, wine at your winery, they first pay the cost of the product, as if it were a sale within Italy, and then separately pay for the shipping abroad.

Many companies believe that with this system, the regulations governing direct sales, as previously discussed, do not apply, and this is completely WRONG.

When does Split Payment not comply with regulations?

- OSS Regime in Europe: If you ship your alcoholic product to the customer’s home, for example, within Europe, the VAT payment must comply with the OSS Regime and its thresholds, requiring the seller to pay VAT in the destination country. Therefore, the sale cannot be treated as a simple sale in Italy. Additionally, VAT under the OSS must also be paid on excise duties, customs duties, and shipping. Here you can find more information on the OSS Regime.

- Payment of Excise Duties and Customs Duties: Alcoholic beverages, being subject to excise duties and customs duties, require specific taxes if shipped to certain countries. Even if the purchase took place in Italy, when shipping the alcoholic product to the customer’s home, for example within the European Union, the excise duty must still be paid.

- Opening and Closing of the Customs Procedure: It is mandatory to open and close the customs procedure for each order sent abroad, with proof of the taxes paid, even if, for example, the excise duty on alcohol for that country is zero.

By separating the cost of the product from the shipping cost, you cannot be sure that your sales comply with these regulations.

Other companies, on the other hand, believe that splitting the payment shifts all responsibility to the end customer or the carrier.

When is Split Payment incorrect for the seller?

Separating the product cost from the shipping cost to circumvent regulations, as mentioned, is completely pointless. This is because, even if the customer pays the shipping cost to the carrier, if the goods are shipped from your company or from an associated warehouse, both the buyer and the seller are responsible for the correct customs and tax management for the shipment abroad.

Most couriers only handle transportation: they are not responsible for the customs and tax management of your sales.

There is only one case in which the seller is not required to fulfill customs obligations.

That is when the foreign customer, after purchasing the alcoholic product, takes it home using their own means. In this case, as stated by the European Excise Duty Code, no customs tax needs to be paid. It will be sufficient to issue a receipt with the Italian VAT for the goods sold.

The absence of customs obligations, however, does not apply when the customer, after purchasing the alcoholic product, independently goes to a shipping company to have the package sent to their home. In this case, the customs and tax obligations for direct sales abroad, which we discussed earlier, must be followed. Since couriers, as a policy, do not handle customs procedures for these shipments, the final customer may be penalized in the event of inspections.

A small consolation, considering that a penalized customer for this type of purchase is a lost customer, especially if you directed them to a shipping company to send the goods without informing them about the applicable regulations and their obligations.

What you have to do?

As mentioned earlier, most carriers do not handle the tax and customs bureaucracy for you in this type of sale.

If you do not have a record of the excise duties, customs duties paid, and the VAT correctly remitted for each order, then you have a problem, and in the event of an inspection, you could face penalties.

The solution, however, exists and is very simple. Get informed about your carriers’ policies and the current regulations for direct sales abroad, so you can use compliant procedures and take full advantage of the D2C channel without worries.